![]()

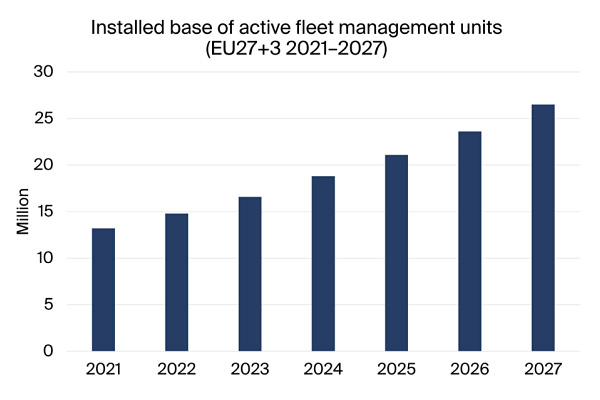

The number of active fleet management systems deployed in commercial vehicle fleets in Europe was 14.8 million at the end of 2022, according to a new research report from the IoT analyst firm Berg Insight.

Growing at a compound annual growth rate (CAGR) of 12.4 percent, this number is expected to reach 26.5 million by 2027. The top-38 vendors have today more than 100,000 active units in Europe.

Berg Insight ranks Targa Telematics as the largest player in terms of active installed base with around 710,000 units at year-end 2022. Weebfleet’s subscriber base has grown both organically and by acquisitions during the past years and the company holds the position as the second largest provider of fleet management solutions on the European market and reached an installed base of about 680,000 units. Verizon Connect is in third place and had achieved an installed base of an estimated 490,000 units at the year-end. Calamp and Radius Telematics follow and have reached 400,000 units and 382,000 units respectively. Scania, ABAX, Gurtam, Bornemann and AddSecure Smart Transport are also ranked among the ten largest providers with 250,000–380,000 units each. Some notable players just outside of the top ten list are MICHELIN Connected Fleet, Geotab, Transics, Quartix, Eurowag Telematics, Viasat, Linqo, Microlise, Daimler Truck, Océan (Orange), Volvo, Macnil, GSGroup, RAM Tracking, MAN, Cartrack, Fleet Complete, Trimble, Optimum Automotive, Shiftmove, AROBS Transilvania Software, Inseego, Infobric Fleet and Mapon. The HCV manufacturers are now growing their subscriber bases considerably thanks to standard line fitment of fleet management solutions. Dynafleet by Volvo, FleetBoard by Daimler Truck and Scania Fleet Management are the most successful with active subscriber bases of 162,000 units, 170,000 units and 379,000 units in Europe respectively at the end of 2022.

The consolidation trend on this market continued in 2023.

Johan Fagerberg, Principal Analyst, said:

“Seven mergers and acquisitions have taken place so far this year among the vendors of fleet management systems in Europe”

In January, Coyote became majority owner of Ubiwan (51 percent). After the change in ownership, the fleet management business of Coyote has now become part of the Ubiwan business. In the same month, Vimcar and Avrios were acquired by Battery Ventures and consequently merged, resulting in a new company called Shiftmove. In February, private equity firm Idico acquired a majority stake in Simpliciti. In May, Targa Telematics acquired Viasat Group. The new larger group will have offices in eight key European countries: Italy, Portugal, Spain, France, the UK, Belgium, Poland and Romania. Mapon acquired CarCops based in Estonia in the same month which will expand the business in the country considerably. Addsecure Smart Transport acquired in October the Clifford Group which includes Traxgo, a Belgium-based company offering systems for tracking of vehicles, machines and equipment. Finally, Powerfleet and MiX Telematics announced in October an agreement to form a combined business which will be branded as Powerfleet. The transaction is expected to close in Q1-2024. Mr. Fagerberg anticipates that the market consolidation of the still overcrowded industry will continue in 2024.